3 Ways to Check Your Credit Score in the US

Stay on top of your credit score with these simple, free checking methods.

Keeping an eye on your credit score might not be a big deal in countries without well-structured financial systems. But in the US, it’s a whole different story—it plays a major role in everything from getting a loan to securing a good interest rate on a credit card.

Luckily, checking your credit score is easier than ever, and in most cases, it won’t cost you a dime. The two main credit scoring models—FICO and VantageScore—offer multiple versions of their scores, all based on reports from the three major credit bureaus: Experian, TransUnion, and Equifax.

There are actually many ways to check your credit score for free, but they typically fall into three main categories.

3 Ways to Check Your Credit Score in the US

1. Check With the Major Credit Bureaus

One of the easiest ways to check your credit score is by going straight to the source—the major credit bureaus. Depending on which one you choose, you might get your score for free or have to pay a small fee.

Here's how each work:

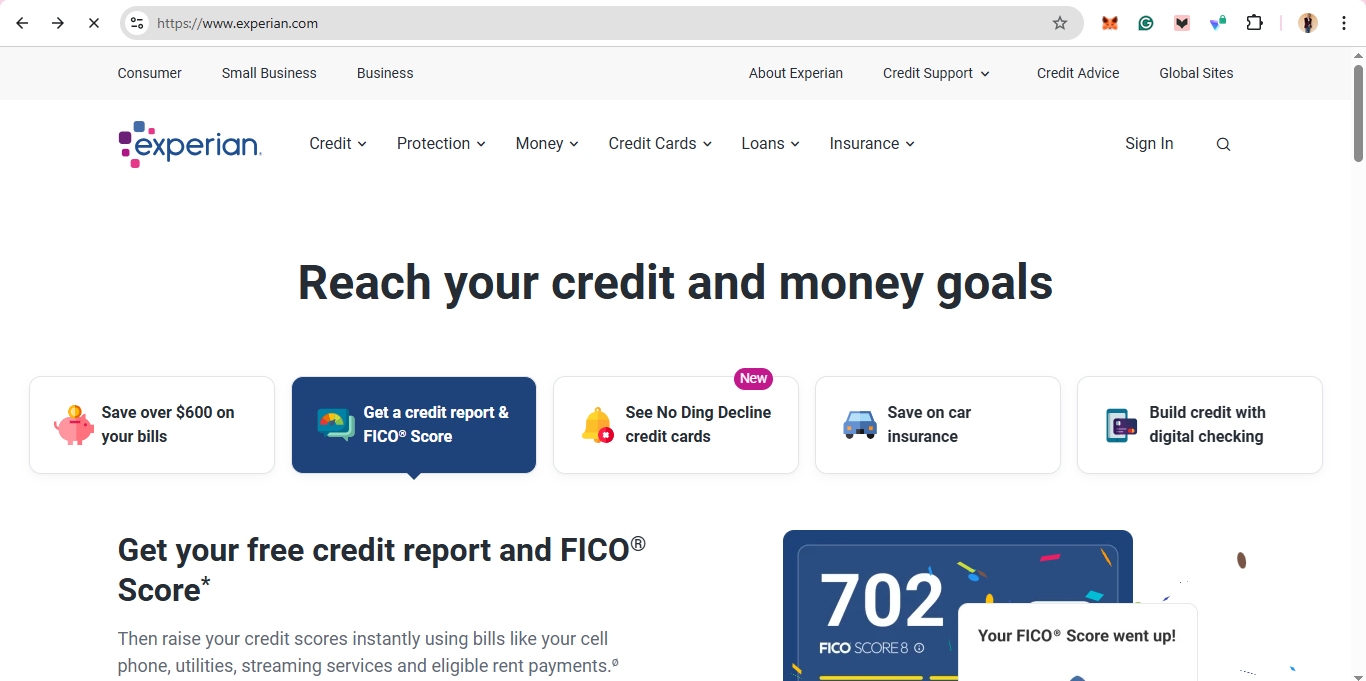

Experian

You can check your credit report and FICO® Score 8 for free anytime with an Experian account. Plus, they offer free credit tracking and alerts, so you’ll know when something changes. You’ll even get personalized tips on improving your score.

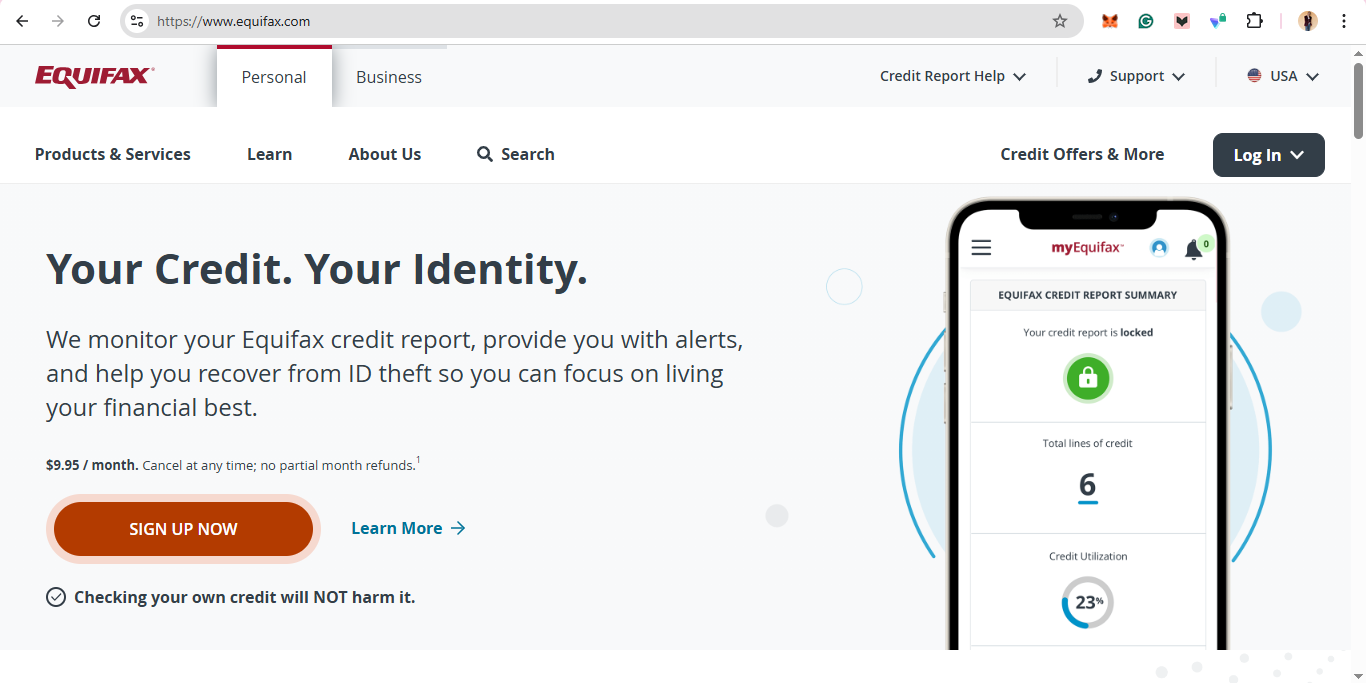

Equifax

With Equifax Core Credit, you can access your Equifax credit report and VantageScore 3.0 for free, updated once a month. If you want extras like alerts and the ability to lock your report, you’ll need to subscribe to Equifax Credit Monitor for $4.95/month.

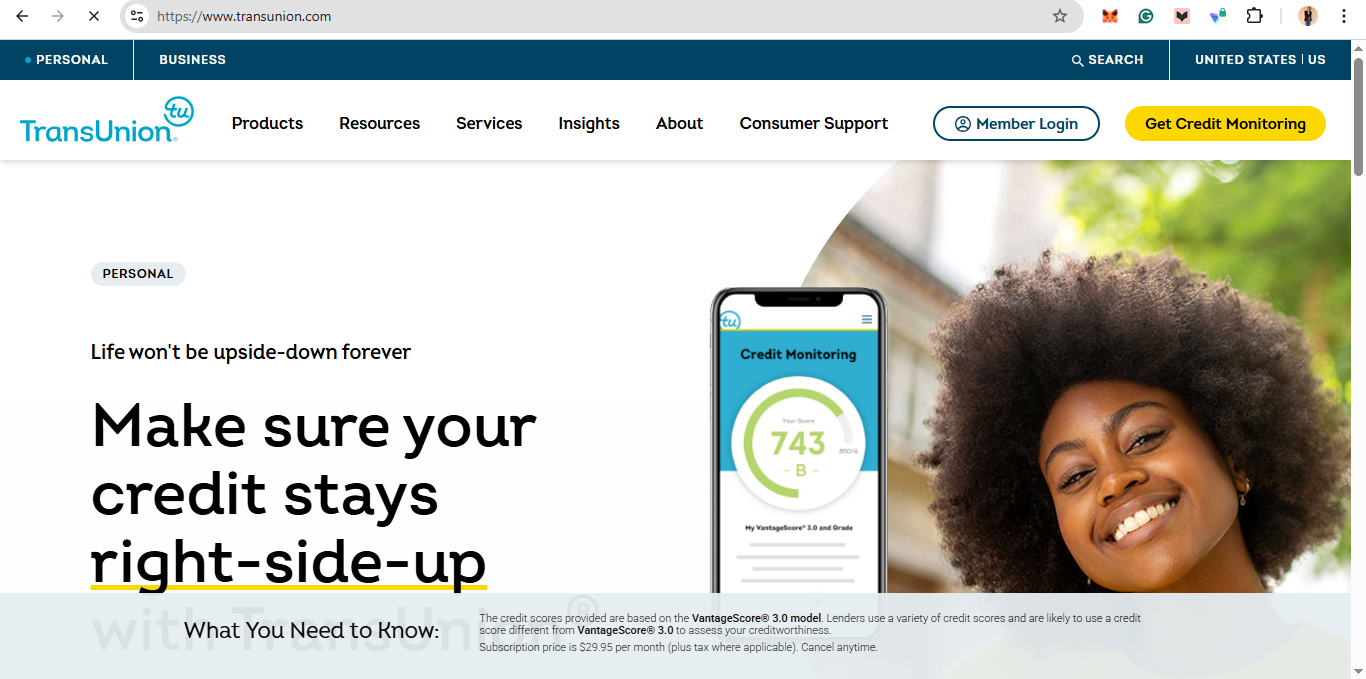

TransUnion

Unlike the other two, TransUnion doesn’t offer free reports or scores directly. If you want access, you’ll have to sign up for their credit monitoring service, which includes a VantageScore 3.0 credit score, at $29.95/month.

2. Use a Free Credit Score Website

Several websites, such as Credit Karma and NerdWallet, let you check your credit score for free—no strings attached. You can also access your full credit report for free through AnnualCreditReport.com, but keep in mind that it won’t include your credit score. These platforms typically make money by offering credit card or loan recommendations based on your score.

At the same time, the type of score and credit report they provide can vary. Since each website calculates your score using its own data, you may notice slight differences between them. Additionally, some lenders report to only one or two credit bureaus, meaning your credit history might look different depending on which agency you use.

3. Check With Your Credit Card Issuer or Lender

If you have a credit card or loan app, there’s a good chance your lender already offers free credit score access. Many banks and card issuers provide either a FICO® Score or a VantageScore through their online banking platforms or mobile apps.

Your score is typically updated monthly, and in some cases, it’s the same score the company uses when evaluating loan or credit card applications. It’s worth checking if your bank or lender offers this perk—sometimes, you’re automatically enrolled, while other times, you’ll need to opt in.

How Credit Score Ranges Impact Your Financial Health

In most cases, credit scores range from 300 to 850, and the higher your score, the better your financial opportunities. A strong credit score can help you qualify for more financial products, secure lower interest rates, and even reduce fees.

Creditors typically categorize credit scores into different groups. While they can set their own thresholds, both FICO and VantageScore offer general benchmarks:

- FICO® Score

- Poor: Below 580

- Fair: 580 – 669

- Good: 670 – 739

- Very Good: 740 – 799

- Excellent: 800+

- VantageScore

- Poor: Below 500

- Fair: 500 – 660

- Good: 661 – 780

- Excellent: 781+

Understanding where you fall within these ranges can help you take steps to improve your score if needed.

Conclusion

Your credit score isn’t just a random number—it’s like your financial reputation, quietly working behind the scenes. If you’ve ever been hit with a higher interest rate than expected or struggled to get approved for a loan, that’s your credit score at play. However, the good news is that keeping tabs on it is easier than ever and doing so can save you from future headaches.

Take a few minutes to check where you stand—you never know, it could be the smartest financial move you make this week.